How housing market inventory is shifting across every state

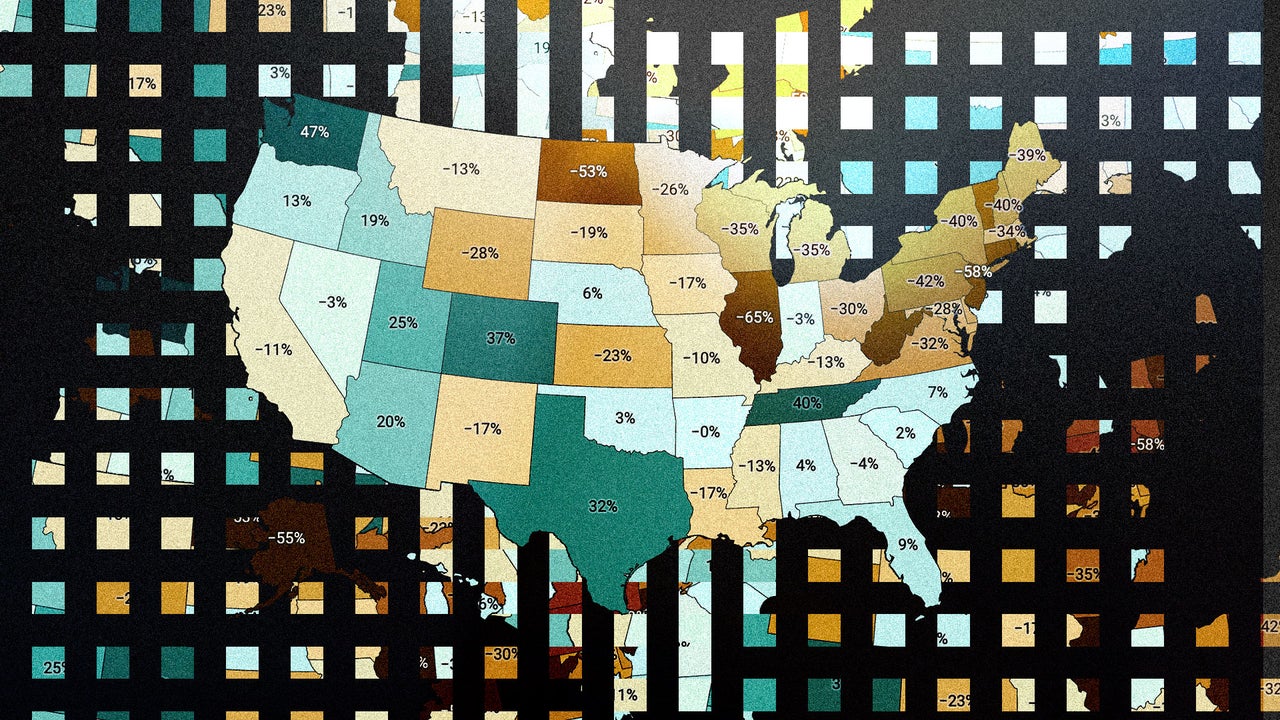

Want more housing market stories from Lance Lambert’s Resi Club in your inbox? Subscribe to the Resi Club newsletter. Speaking in front of institutional investors and money managers on Tuesday at the Bank of America Housing Symposium, Pulte Group’s VP of investor relations, Jim Zeumer, said America’s third-largest homebuilder still has “work to do in Oregon and Washington. … We have work to do to clear spec in some of our Western markets.” By “work,” he means making affordability adjustments to better align with market conditions in PulteGroup’s Oregon and Washington communities. While the state of Washington has seen active inventory rise 17% year over year, nationally aggregated inventory has slowed way down—up just 2.2% on a year-over-year basis between May 31, 2025, and May 31, 2026. If you go back 12 months, that year-over-year national inventory growth rate was much higher (31.5%). After a period of softening in which leverage shifted more toward homebuyers, the supply-demand balance in the nationally aggregated housing market has been more stable in recent months, settling into what ResiClub considers a “soft” market. Again, for that comment, ResiClub is talking about the nationally aggregated market—regionally and locally, there’s a lot of nuance. Nationally, we’re still below pre-pandemic 2019 inventory levels (10.4% below May 2019). And some resale markets—in particular chunks of the Midwest and Northeast—remain, relatively speaking, tight-ish. May inventory/active listings total, according to Realtor.com: May 2017 -> 1,253,854 May 2018 -> 1,156,910 May 2019 -> 1,180,920 May 2020 -> 928,370 May 2021 -> 447,662 (Pandemic housing boom overheating) May 2022 -> 479,462 (Pandemic housing boom overheating) May 2023 -> 582,441 May 2024 -> 787,722 May 2025 -> 1,036,101 May 2026 -> 1,058,693 Between May 2024 and May 2025, U.S. active inventory across the country rose by 248,379 homes for sale. Between May 2025 and May 2026, U.S. active inventor