Mortgage rate: 6.5% If indexed: 1.2% Why not indexed? Superstition.

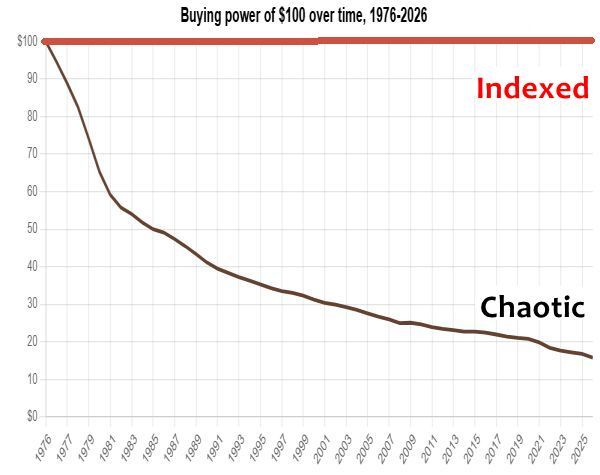

Of course the headline sounds preposterous; it is preposterous. But it's true, and there's no trick. People have been explaining this fervently for 204 years; I've been one of them for 41 years. I'll eventually be presenting a history of what kept the news from those whose lives it would have changed, with such lessons as I see, but for now here's enough to get the ball rolling: a few quotes and links, followed by an explanation of what the "nominal interest rate" is, and how wealth-measure finance (to name it after the desired effect rather than the technique of indexing) works.Thumbs up from 3 Nobelists:Milton Friedman, How to Save the Housing Industry Newsweek, 1980:The greater part of the payments designated 'interest' have really been a repayment of principal... the mislabeling of principal payments as interest payments... prices housing out of the reach of many. If the 14% were correctly labeled... the effective interest rate would be 4%.Franco Modigliani, New Mortgage Designs For Stable Housing In An Inflationary Environment, 1975, p35PLAM (price level adjusted mortgage: his term for "indexed") does appear to offer a more complete solution... through a contract which, in effect, produces the same real effect as would the traditional mortgage in the absence of inflation - and does so no matter what the rate of inflation either anticipated or realized.Robert Shiller, Public Resistance to Indexation: A Puzzle, 1997The indexation of payments makes excellent sense for all sorts of long-term contracts. Future payments should not be expressed in currency units, but instead tied to an index of consumer prices or an index of wholesale prices, of wages, of incomes, or of components of income. History shows that the real value of currency units has been so unstable that it is better to use practically any one of these indexes to specify future payments in contracts than to specify payments in terms of fixed currencyThe mechanism of false interest: Clawback and TOFLIClaw